When taxes absolutely can't be avoided, clients want to know their best option; how to keep the cost as low as possible, who should pay these costs, and when. Consider:

Capital Gains exemptions having been the focus of considerable tax changes over the past decade or so, yet despite the bad news, many Canadians have used old financial products in a new light, essentially 'buying another capital gains exemption'. The plan is appropriate for assets they intend to keep in the family, such as the family cottage. Capital Gains exemptions having been the focus of considerable tax changes over the past decade or so, yet despite the bad news, many Canadians have used old financial products in a new light, essentially 'buying another capital gains exemption'. The plan is appropriate for assets they intend to keep in the family, such as the family cottage.

It started in 1988-89, when the taxable portion of capital gains increased by 50%. Later in 1989, the personal capital gains exemption was reduced by $400, 000. to a mere $100, 000. In 1994, the personal exemption was wiped out entirely. This meant Canadians would now pay taxes on all capital gains. More recently, the focus has been on reductions, two in 2000 alone.

In the case of a cottage, this can have significant tax implications. Using a growth rate of 5%, a 55 year old can expect the fair market value (fmv) of the cottage to quadruple within his or her lifetime. When an owner dies, the property is deemed to be sold at the fmv and capital gains tax is calculated on the difference between this and the adjusted cost base (acb). The tax is payable even though the cottage was never actually sold.

Taxes can be deferred using the spousal capital rollover provision or by ensuring the cottage is in joint tenancy ownership with a spouse. In either case, tax is deferred to the death of the surviving spouse, and the acb is retained, meaning the tax bill will continue to grow during the deferral.

The time to look at alternatives is now. Waiting means later being reactive and leaves no way to be pro-active.

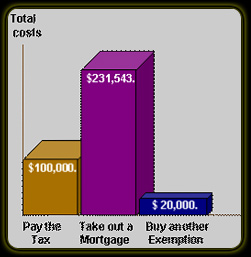

When the tax comes due there are three options. One is to pay it, which might require the property actually be sold and numerous other costs incurred.

Another is to take a mortgage, which adds the non-deductible interest expense to the taxes and encumbers it over the amortization period.

The third is to pay it using the proceeds of life insurance, which can be structured to pay out exactly when the tax bill is expected, ideally at the second death of a couple. This graph shows the cost comparison assuming a couple, aged 65, gain of $400, 000, marginal tax rate of 50%, 8% mortgage over 25 years and net investment rate of 6%:

As for who should pay, the logical answer is whoever would have paid the mortgage in the above alternative.

|